Featured Topics

Private Credit vs. Equity: How to Think About Yield

")

What “Downside Protection” Actually Means

Why Real Estate Beats Cash During Inflationary Cycles

News & Updates

Track the latest from Alpha Equity Group including fund openings, market insights, and performance updates.

At Alpha Equity Group, we believe in a simple but powerful real ...

Rent Control: A Well-Intentioned Policy That Misses the Mark

In the ...

In the world of capital markets, clarity is often fleeting — and ...

When markets break from fundamentals, the prudent real estate investor ...

Understanding and evaluating investment opportunities requires more than ...

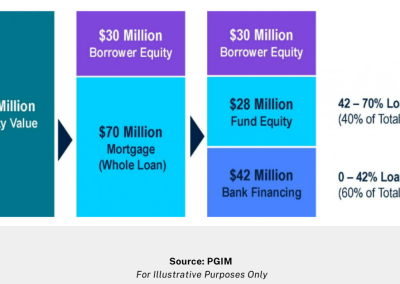

I n today’s market, lending to your own projects can understandably ...

In the world of CRE valuations, many investors get hung up on cap rates - ...

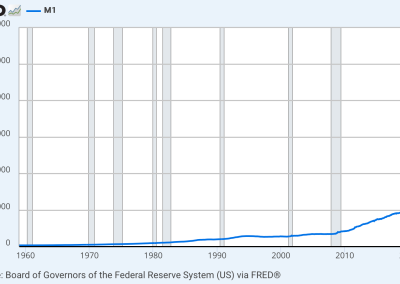

Simply put, the Fed’s Balance Sheet materially impacts the CRE ...

As you may already be aware, the Trump administration has implemented ...

The fundamental need for housing is universal—everyone requires a ...

Price discovery in commercial real estate (CRE) is influenced by a range ...

Historical / Foundational Context

Historically, banks have been one of ...

No results found.

Frequently Asked Questions

Investor-focused answers to our most common questions.

Who can invest with Alpha Equity?

Only accredited investors as defined by the SEC.

What is the minimum investment?

Catalyst Fund: $50,000. Other opportunities may vary.

What types of returns are expected?

Catalyst targets 10–12% preferred return, paid monthly.

When can I redeem my investment?

Redemptions allowed after 12 months, with 120-day notice and quarterly liquidity limits.

Do you charge fees?

Catalyst charges no management or performance fees.

What is a 721 Exchange?

A structure allowing real estate owners to contribute property in exchange for LP units avoiding capital gains tax at the time of contribution.