Investments

Performance

About

Firm Overview

Investment Strategy

Team

Holdings

Resources

Insights

Education Center

FAQ

Login

Get Started

Investments

Performance

About

Firm Overview

Investment Strategy

Team

Holdings

Resources

Insights

Education Center

FAQ

Get Started

Login

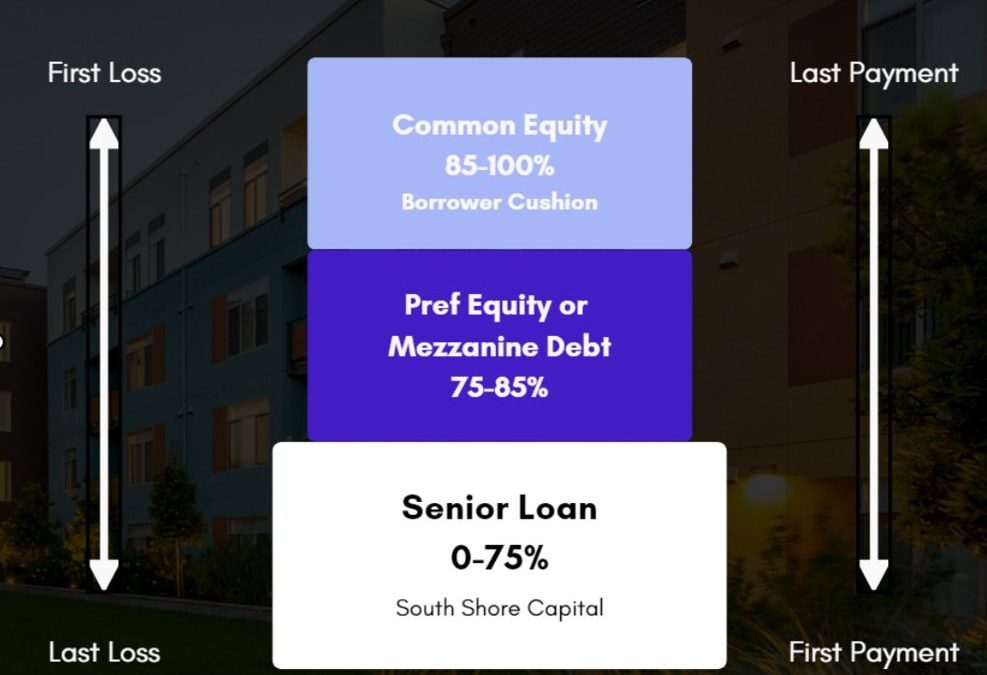

The-Capital-Stack

Jan 28, 2026

Recent Posts

Thinking Big with Taylor Lyles

October 13, 2025

Coker Creek Estates

October 13, 2025

Tiny Home Open House: Farmers Cove

October 13, 2025

Building to Hold vs Building to Sell

July 31, 2025

Rent Control – Does it Work?

July 31, 2025

Categories

Advanced Investing Topics

Blog

Capital Markets

Deals

Events

Market Monitor

Real Estate Investing